The Importance of Reconciling and Auditing Transactions

Key Takeaways

- Reconciliation gap: FCA data suggests transaction reporting errors remain widespread, while limited uptake of reconciliation data requests indicates many firms still lack effective assurance processes.

- Hidden obligation: MiFID II requires firms to reconcile reports against front office records, not merely rely on ARM submissions or downstream reporting workflows.

- Supervisory risk: Low use of the FCA’s MDP reconciliation data may give supervisors a simple way to identify firms struggling with core transaction reporting duties.

- Operational challenge: Effective reconciliation requires comparing raw front office data with regulator-bound reports, which exposes missing submissions and clarifies why breaks occurred.

- Control design: Independent reconciliation tools can provide more credible evidence of reporting validity and reduce the risk of firms effectively marking their own homework.

After more than two years, financial service firms are getting their collective head's around the transaction reporting regime. Or at least that is what we would like to think. An FOI request from the FCA reveals a different picture:

- 15% of UK investment firms have admitted errors in transaction reporting to the FCA

- 223 firms have been contacted by the FCA about possible reporting errors

These figures imply that about 20% of firms have been in discussion with the FCA regarding transaction reporting errors. But this may only be the tip of the iceberg.

The MiFID 2 requirements include the obligation to reconcile the data held in a firm's front office system with the data sent to their competent authority as stated in Article 15 of this Delegated Regulation:

The solution the FCA has provided for this is the MDP (Market Data Processor) system. A firm registers with the FCA and requests a sample of transaction report data to use in a reconciliation. As of November 2019, only 18% of MiFID firms had requested reconciliation data. This must surely present a red flag and an easy target for the FCA to use to identify firms that are struggling with transaction reporting obligations.

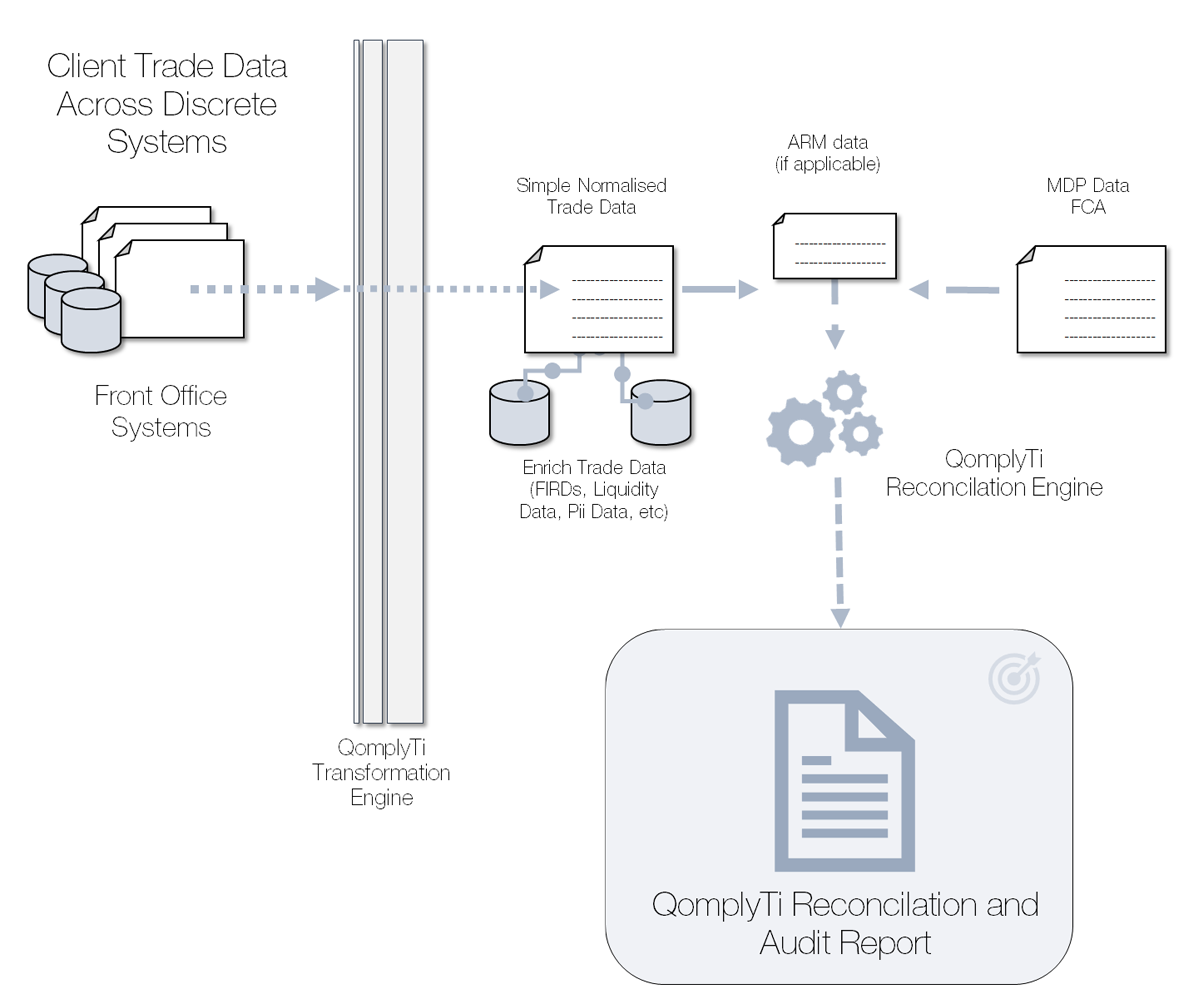

Front Office Systems

An important point to note is that the regulation requires a reconciliation with Front Office systems. This is not necessarily the same data as that provided to an ARM. The implication of the regulation is that reconciliation is to take place between the raw transaction data as entered by front office staff that has not been processed before submission to an ARM. This would give firms to opportunity to identify transactions that are not being reported and establish why that is the case.

The reconciliation process looks like this:

This mandated reconciliation process appears to have slipped under the radar of a lot of firms. The use of an ARM does not address the requirement to reconcile directly with a firm's front office systems. Firms need to address this issue themselves.

Practically, firms face reconciling their data against yet another data format. Once a reconciliation is produced, the results should be actionable and aid in any required back reporting. There may be an advantage in using a tool specially designed to reconcile transaction reports. Generic reconciliation tools can take a considerable amount of effort to set up and will impact on already stretched development teams. And the use of an independent tool may reduce the risk of 'marking your own homework' and give a true reflection of transaction reporting validity.

How Qomply can help

Qomply’s Regulatory Reporting Hub combines regulatory expertise with AI, automation and data analytics to deliver scalable, audit-ready reporting intelligence that reduces errors, lowers remediation costs, and minimises operational and regulatory risk.

Covering regimes including MiFIR, EMIR Refit, SFTR, CFTC, CSA, MAS, ASIC and HKMA, Qomply also offers a fully managed service and operates globally from London.

Frequently asked questions

-

The FCA FOI data suggests transaction reporting issues are more widespread than many firms may assume. The article says 15% of UK investment firms admitted errors, 223 firms had been contacted by the FCA about possible reporting errors, and around 20% of firms may already have been in discussion with the regulator.

-

Article 15 requires firms to reconcile the data in their front office systems with the data sent to their competent authority. The article presents this as a direct MiFID II obligation rather than an optional control.

-

The FCA's Market Data Processor (MDP) is the mechanism firms use to obtain transaction report samples for reconciliation. The article explains that firms must register with the FCA and request sample data through MDP to perform the check.

-

The article stresses that the regulation requires reconciliation against front office systems, not just data passed to an ARM. It says this helps firms identify transactions that were never reported and understand why they were missed.

-

Firms should put in place a framework for periodic transaction report reconciliations now. The article warns that the FCA monitors requests for data extracts, which makes it relatively easy to identify firms that are not complying.

Purpose-built solutions and services for regulatory reporting

Designed to improve accuracy, reduce risk, and support confident transaction reporting.